Credit Crib Notes: Anywhere Real Estate (HOUS)

We summarize the financial and operating trends for HOUS in bullets and charts.

Credit quality trend: Negative, especially for unsecured. Plunging volumes in existing home sales undermines commissions while structural subordination risks are rising for unsecured at a time of high legal contingent liability risks and near-term trial dates for major antitrust class action cases.

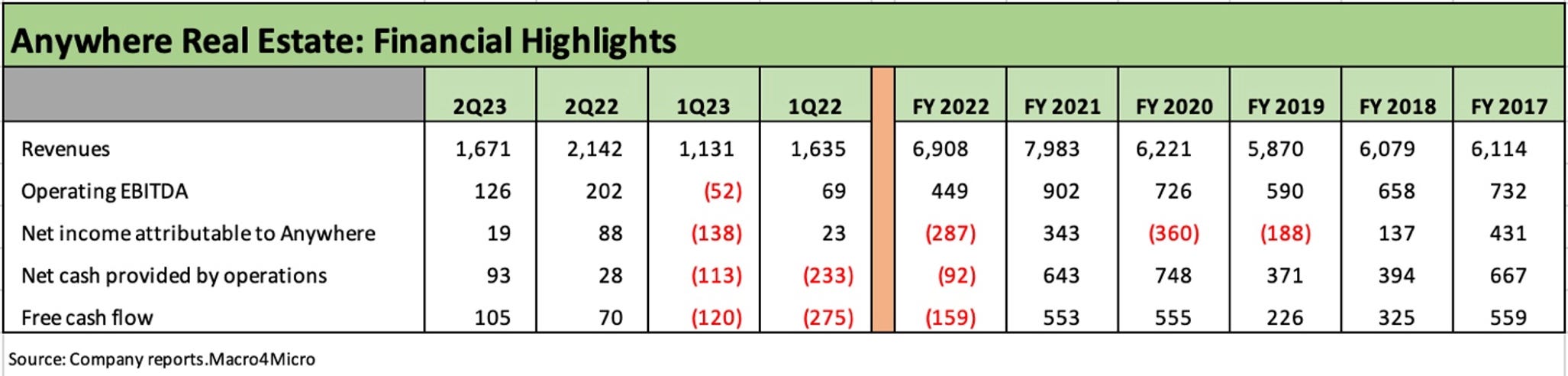

Operating results: Despite resilient home prices, commissions/fees are down across franchise operations, the owned brokerage group, and in title services, in turn setting the stage for very tight cash flows in 2023.

Financial profile: Earnings, cash flow, and leverage trends show rising financial risk even as legal claims exposure is rising and more assets in a brand oriented services company are getting encumbered in debt exchanges.

The overriding revenue and cost variables have been mixed with volumes down materially on strained affordability tied to mortgages rates in turn driving weak earnings and cash flow with revenue weakness partially offset by cost-cutting and restructuring actions.

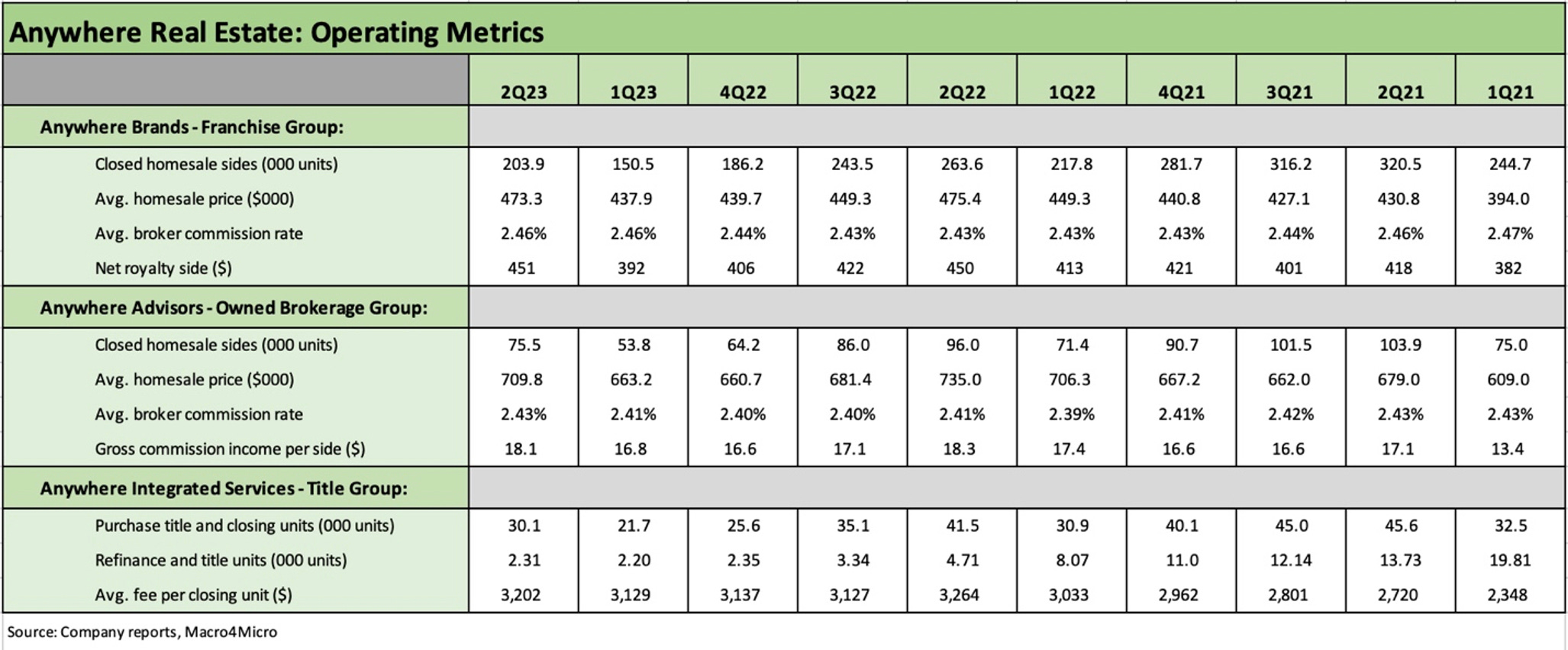

Franchise royalties are paid to the Franchise Group including high intercompany royalty payments by the Owned Brokerage Group.

EBITDA rebounded in the seasonally strong 2Q23 period but sustaining cash flow will require more successful cost cutting and improvement in existing home sales volumes with the typical peak selling season underway and a seasonal slowdown ahead in 4Q23 and 1Q24.

The operating metrics show price and volume trends for a company that ranks among the largest residential real estate brokers.

HOUS is facing weakness in existing home sales volume (“sides” for buys and sells) that could stay soft as mortgage rates reach new cyclical highs over 7%.

Revenue is driven by (sides x price x commission rate) with the negative variance in 2Q23 tied to -23% in Franchise Group sides and -21% in Owned Brokerage Group sides.

Average prices for 2Q23 only declined by -0.5% in “Franchise” and -3.4% in “Owned Brokerage.”

Title volumes were driven by lower home sales and lower mortgage refinancing.

Generally, new franchise agreements have a term of 10 years and cannot be terminated with ~6% of franchise commissions paid to HOUS (subject to some performance-based metrics).

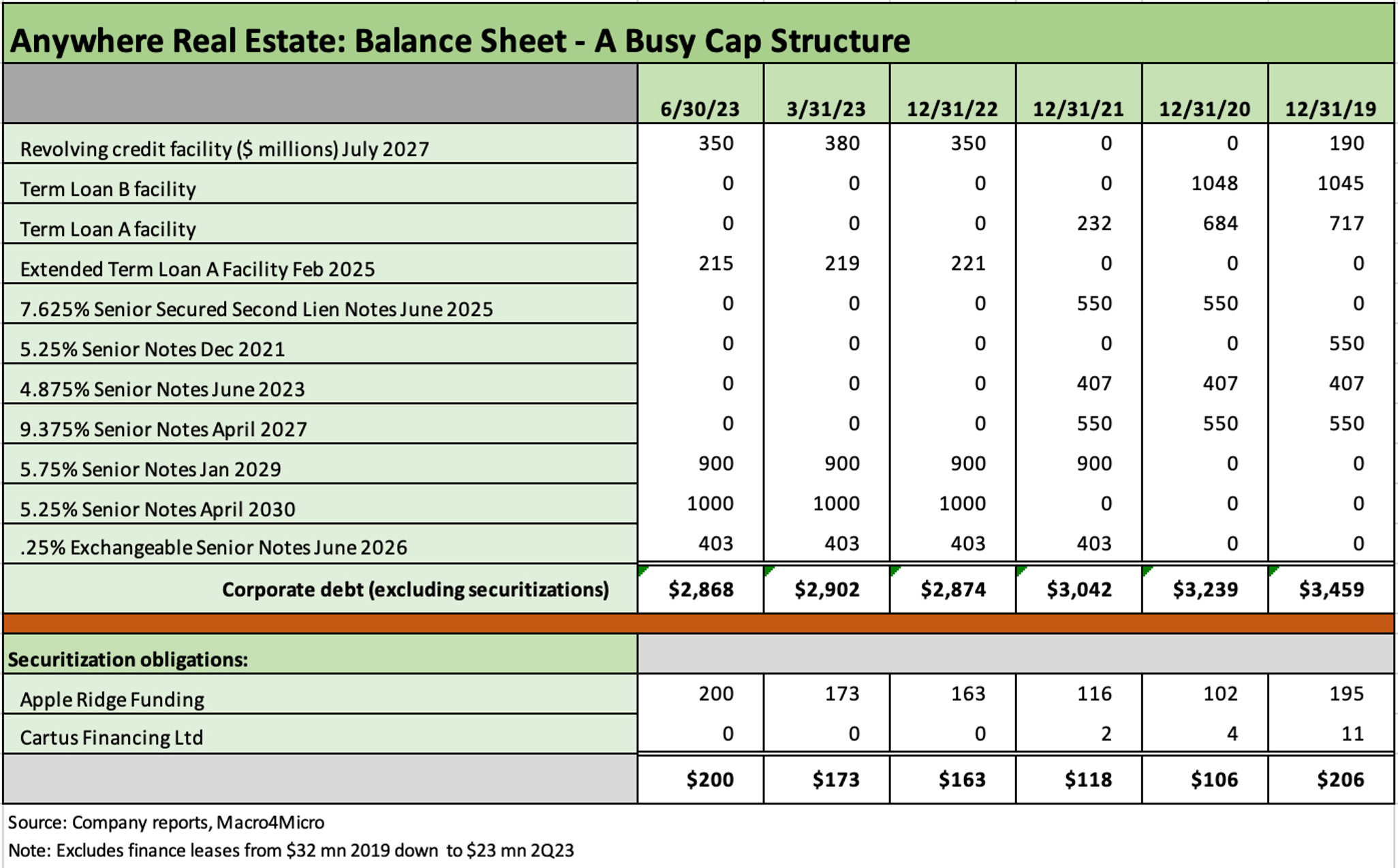

The capital structure evolution of HOUS from a 2007 LBO to a post-IPO single B issuer has been a busy liability management process around bouts of credit selloffs and rallies.

At 2Q23, HOUS had $1.1 bn of borrowing capacity under its revolver (matures July 2027 but a springing date of March 2026 subject to bond refi terms on Exch Sr Notes) with $350 mn borrowed ($310 as of 10Q filing) and $36 mm LOCs.

Term Loan A amortizes to a maturity date of Feb 2025.

Securitization obligations of $200 mn are fully utilized and expire in May 2024 after being renewed in June 2023.

The refinancing wave of 1Q21 ($900 mn unsecured 5.75% of Jan-Fed 2019) and 1Q22 ($1 bn unsecured of 5.25% 2030 in Jan 2022) allowed HOUS to extend liabilities, refi high coupon debt (9.375% of 2027), and clean up liens (7.625% 2L of 2025).

Demand for HOUS unsecured debt in 2021/early 2022 came before the Fed hiking cycle and after a very strong period for existing home sales and mortgage refinancing that saw HOUS generate over $900 mn in EBITDA FY 2021.

The shift to a heavily unsecured capital structure in 2022 made room for exchanges into 2L in the current troubled market of 2023 and with exchanges at a 20 point haircut to face value.

Subsequent to 2Q23, HOUS agreed to debt exchange offers for bondholders swapping from unsecured to 2L with the exchange potentially reflecting concerns over unsecured legal claims risk.

A heavy weighting of longer-dated unsecured bonds maturing in 2029-2030 gave HOUS room to maneuver in executing on the exchanges including the initial exchange $273 mn of 2029/2030 bonds for $218 mn 7% 2L bonds due 2030 at 80 cent on the dollar..

With its subsequent additional exchange offers, HOUS offered to exchange up to $640 mn in new notes for up to $800 mn in old notes.

Weak cash flow and structural subordination will likely take unsecured bonds into the CCC tier as legal claims risk from pending class action litigation threatens asset coverage.

Highlights and History

Anywhere (name change from Realogy in 2022) boasts leading brands including Coldwell Banker, Century 21, ERA, Sotheby’s International, Corcoran, and Better Homes and Gardens.

Realogy was spun off from Cendant in 2006, LBO’d by Apollo (April 2007), and did an IPO in Oct 2012 (posting a -82% total return from the IPO through 8-23-23).